Attack or defense? An example of multiple regression#

What should you pay for, if you want to win the English Premier League?

import numpy as np

import pandas as pd

pd.set_option('mode.copy_on_write', True)

import matplotlib.pyplot as plt

# Show arrays without exponential notation, 6 digits of precision.

np.set_printoptions(suppress=True, precision=6)

<Token var=<ContextVar name='format_options' default={'edgeitems': 3, 'threshold': 1000, 'floatmode': 'maxprec', 'precision': 8, 'suppress': False, 'linewidth': 75, 'nanstr': 'nan', 'infstr': 'inf', 'sign': '-', 'formatter': None, 'legacy': 9223372036854775807, 'override_repr': None} at 0x7fa3d06db330> at 0x7fa3d6585d40>

# For minimize.

import scipy.optimize as spo

# For linregress

import scipy.stats as sps

# For running statistical models.

import statsmodels.formula.api as smf

We load the data on wage spends in the 2021-2022 English Premier League (EPL).

See the EPL dataset page for more details.

df = pd.read_csv('data/premier_league_2021.csv')

df.head()

| rank | team | played | won | drawn | lost | for | against | goal_difference | points | wages_year | keeper | defense | midfield | forward | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | Manchester City | 38 | 29 | 6 | 3 | 99 | 26 | 73 | 93 | 168572 | 8892 | 60320 | 24500 | 74860 |

| 1 | 2 | Liverpool | 38 | 28 | 8 | 2 | 94 | 26 | 68 | 92 | 148772 | 14560 | 46540 | 47320 | 40352 |

| 2 | 3 | Chelsea | 38 | 21 | 11 | 6 | 76 | 33 | 43 | 74 | 187340 | 12480 | 51220 | 51100 | 72540 |

| 3 | 4 | Tottenham Hotspur | 38 | 22 | 5 | 11 | 69 | 40 | 29 | 71 | 110416 | 6760 | 29516 | 30680 | 43460 |

| 4 | 5 | Arsenal | 38 | 22 | 3 | 13 | 61 | 48 | 13 | 69 | 118074 | 8400 | 37024 | 27300 | 45350 |

Notice that we have the total yearly wage bill for each team, as well as the individual spends on the keeper, defense, midfield and forwards.

There are 20 EPL teams.

len(df)

20

The data frame describe method gives useful statistics for all the numerical columns.

df.describe()

| rank | played | won | drawn | lost | for | against | goal_difference | points | wages_year | keeper | defense | midfield | forward | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 20.00000 | 20.0 | 20.000000 | 20.0000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.00000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.00000 |

| mean | 10.50000 | 38.0 | 14.600000 | 8.8000 | 14.600000 | 53.550000 | 53.550000 | 0.000000 | 52.60000 | 91201.650000 | 7826.900000 | 28240.350000 | 20573.600000 | 34560.80000 |

| std | 5.91608 | 0.0 | 6.762124 | 3.5333 | 6.451438 | 19.454332 | 16.223683 | 33.829293 | 19.34561 | 56966.366691 | 6188.993744 | 15652.908004 | 13186.983145 | 26175.61029 |

| min | 1.00000 | 38.0 | 5.000000 | 3.0000 | 2.000000 | 23.000000 | 26.000000 | -61.000000 | 22.00000 | 28606.000000 | 2080.000000 | 8686.000000 | 3980.000000 | 6280.00000 |

| 25% | 5.75000 | 38.0 | 10.500000 | 6.0000 | 11.750000 | 42.000000 | 43.750000 | -20.000000 | 39.75000 | 47872.500000 | 3065.000000 | 14925.000000 | 11747.500000 | 17805.50000 |

| 50% | 10.50000 | 38.0 | 13.000000 | 8.0000 | 14.500000 | 49.000000 | 53.500000 | -2.000000 | 50.00000 | 75622.000000 | 7410.000000 | 26718.000000 | 16386.000000 | 26410.00000 |

| 75% | 15.25000 | 38.0 | 17.250000 | 11.0000 | 18.000000 | 61.250000 | 63.000000 | 10.000000 | 60.75000 | 112330.500000 | 9462.500000 | 32890.000000 | 28145.000000 | 41129.00000 |

| max | 20.00000 | 38.0 | 29.000000 | 15.0000 | 27.000000 | 99.000000 | 84.000000 | 73.000000 | 93.00000 | 238780.000000 | 28600.000000 | 60480.000000 | 51100.000000 | 112780.00000 |

Notice mean (and sum) goal_difference is 0. This must be so, because every

goal counts 1 positive for the scoring team, and 1 negative for the other team.

The shape attribute of the data frame gives the number of rows and the number of columns.

df.shape

(20, 15)

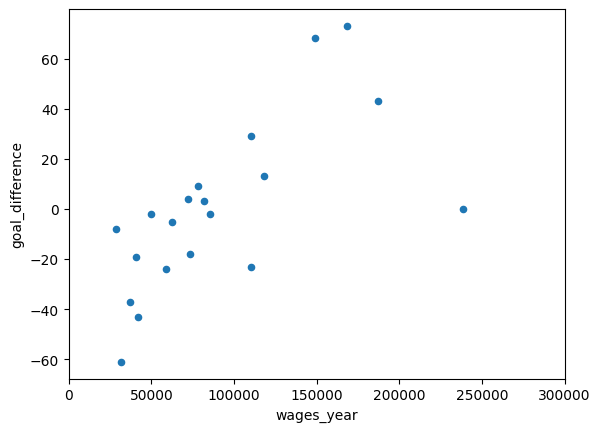

We are interested in whether the wage spend can predict the goal difference. Maybe if you pay more, you score more goals and keep more goals out.

df.plot.scatter(x='wages_year', y='goal_difference')

# We show the y-axis so we can estimate the intercept.

plt.xlim(0, 300000)

(0.0, 300000.0)

We want a best-fit line to these data.

We can use a cost-function to tell use the quality of the line. Low cost corresponds to a good line.

We use the usual sum-of-squared errors as the cost.

def sse_cost(params, x, y):

""" Sum of squared error cost function

"""

b, c = params

y_hat = b * x + c

errors = y - y_hat

return np.sum(errors ** 2)

Here are some estimates for the intercept and slope, by eye-balling the graph.

guessed_intercept = -40

# Goal difference increases by about 20 for a £50,000 increase in spend.

# Slope is rise (in y) divided by run (over x).

guessed_slope = 20 / 50000

guessed_slope

0.0004

We use minimize and the 'powell' method to find the values for slope and intercept (params) that give the lowest values for the cost function.

res = spo.minimize(sse_cost, [guessed_intercept, guessed_slope],

method='powell',

args=(df['wages_year'], df['goal_difference']))

res

message: Optimization terminated successfully.

success: True

status: 0

fun: 12070.170784478678

x: [ 3.728e-04 -3.360e+01]

nit: 34

direc: [[ 5.352e-07 1.264e-01]

[ 8.769e-07 8.421e-02]]

nfev: 833

These are the parameters (the slope and the intercept):

res.x

array([ 0.000373, -33.601334])

If we run linregress, this uses the mathematics of sum-of-squares to get the

minimizing slope and intercept.

lr_res = sps.linregress(df['wages_year'], df['goal_difference'])

lr_res

LinregressResult(slope=np.float64(0.00039689691255513594), intercept=np.float64(-36.197653304934114), rvalue=np.float64(0.6683490305377195), pvalue=np.float64(0.0012767215478024995), stderr=np.float64(0.0001041171418862387), intercept_stderr=np.float64(11.11698541165042))

We suspect that minimize was less accurate than sps.linregress; the very

small slope may mean that minimize gives up searching for the exact correct

slope when it has got very close.

Here’s the cost function value from the parameters from minimize.

sse_cost(res.x, df['wages_year'], df['goal_difference'])

np.float64(12070.170784478678)

The parameters from sps.linregress are slightly better — they give a somewhat lower value for the cost function.

sse_cost([lr_res.slope, lr_res.intercept], df['wages_year'], df['goal_difference'])

np.float64(12031.163363559293)

In data science practice, we often use these least-squares cost functions, and we can use convenient libraries for these calculations. statsmodels is a useful library for these general models.

Using statsmodels, we first create a model, that encodes the relationship

we’re investigating, along with the data.

sm_model = smf.ols('goal_difference ~ wages_year', data=df)

sm_model

<statsmodels.regression.linear_model.OLS at 0x7fa39854b710>

Once we have specified this model, we can use the .fit method of the new

model to calculate the least-squares parameters.

sm_fit = sm_model.fit()

sm_fit

<statsmodels.regression.linear_model.RegressionResultsWrapper at 0x7fa37f780b90>

Finally, we can use the .summary method of the fit result, to show a detailed

display of the parameters and other calculations from the fit.

sm_fit.summary()

| Dep. Variable: | goal_difference | R-squared: | 0.447 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.416 |

| Method: | Least Squares | F-statistic: | 14.53 |

| Date: | Tue, 03 Sep 2024 | Prob (F-statistic): | 0.00128 |

| Time: | 10:05:32 | Log-Likelihood: | -92.374 |

| No. Observations: | 20 | AIC: | 188.7 |

| Df Residuals: | 18 | BIC: | 190.7 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -36.1977 | 11.117 | -3.256 | 0.004 | -59.554 | -12.842 |

| wages_year | 0.0004 | 0.000 | 3.812 | 0.001 | 0.000 | 0.001 |

| Omnibus: | 1.288 | Durbin-Watson: | 1.194 |

|---|---|---|---|

| Prob(Omnibus): | 0.525 | Jarque-Bera (JB): | 0.487 |

| Skew: | -0.375 | Prob(JB): | 0.784 |

| Kurtosis: | 3.142 | Cond. No. | 2.05e+05 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 2.05e+05. This might indicate that there are

strong multicollinearity or other numerical problems.

Defense or attack?#

Here’s a reminder of the columns of data we have.

df.head()

| rank | team | played | won | drawn | lost | for | against | goal_difference | points | wages_year | keeper | defense | midfield | forward | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | Manchester City | 38 | 29 | 6 | 3 | 99 | 26 | 73 | 93 | 168572 | 8892 | 60320 | 24500 | 74860 |

| 1 | 2 | Liverpool | 38 | 28 | 8 | 2 | 94 | 26 | 68 | 92 | 148772 | 14560 | 46540 | 47320 | 40352 |

| 2 | 3 | Chelsea | 38 | 21 | 11 | 6 | 76 | 33 | 43 | 74 | 187340 | 12480 | 51220 | 51100 | 72540 |

| 3 | 4 | Tottenham Hotspur | 38 | 22 | 5 | 11 | 69 | 40 | 29 | 71 | 110416 | 6760 | 29516 | 30680 | 43460 |

| 4 | 5 | Arsenal | 38 | 22 | 3 | 13 | 61 | 48 | 13 | 69 | 118074 | 8400 | 37024 | 27300 | 45350 |

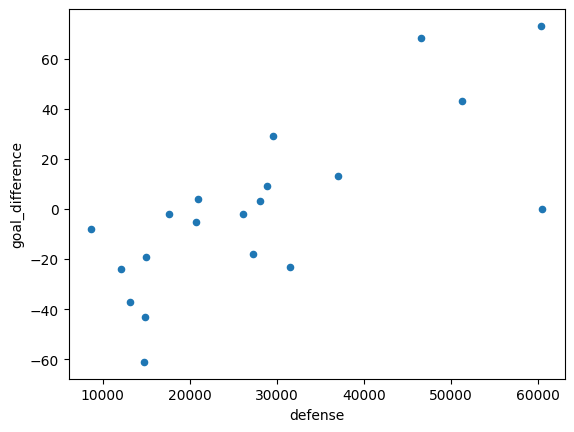

Our question now is — should we spend on defense, or spend on attack (forwards)?

Here’s the plot of defense spending as a function of goal difference.

df.plot.scatter(x='defense', y='goal_difference')

<Axes: xlabel='defense', ylabel='goal_difference'>

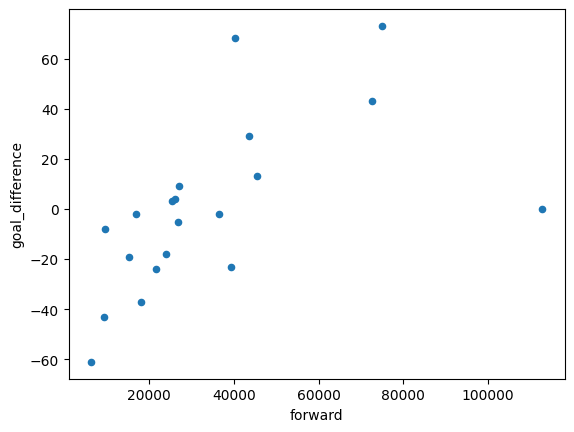

And the relationship of forward spending and goal difference.

df.plot.scatter(x='forward', y='goal_difference')

<Axes: xlabel='forward', ylabel='goal_difference'>

Notice that both, on their own, have strongly positive relationships.

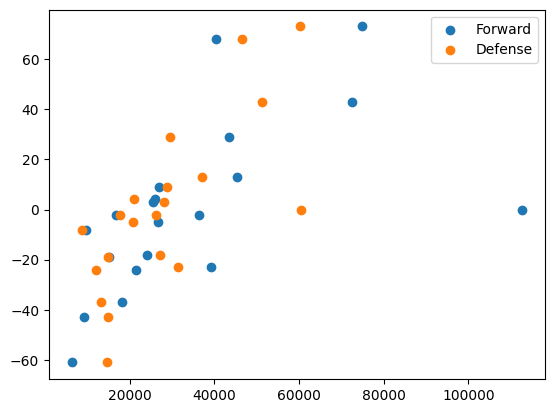

Here we put both on the same plot.

plt.scatter(df['forward'], df['goal_difference'], label='Forward')

plt.scatter(df['defense'], df['goal_difference'], label='Defense')

plt.legend()

<matplotlib.legend.Legend at 0x7fa37d6432d0>

Here we calculate the simple regression models for each. Notice the chained execution for calculating the model, then the fit, and then the summary.

smf.ols('goal_difference ~ defense', data=df).fit().summary()

| Dep. Variable: | goal_difference | R-squared: | 0.549 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.524 |

| Method: | Least Squares | F-statistic: | 21.94 |

| Date: | Tue, 03 Sep 2024 | Prob (F-statistic): | 0.000185 |

| Time: | 10:05:32 | Log-Likelihood: | -90.322 |

| No. Observations: | 20 | AIC: | 184.6 |

| Df Residuals: | 18 | BIC: | 186.6 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -45.2366 | 10.976 | -4.121 | 0.001 | -68.297 | -22.176 |

| defense | 0.0016 | 0.000 | 4.684 | 0.000 | 0.001 | 0.002 |

| Omnibus: | 1.906 | Durbin-Watson: | 1.356 |

|---|---|---|---|

| Prob(Omnibus): | 0.386 | Jarque-Bera (JB): | 1.197 |

| Skew: | -0.597 | Prob(JB): | 0.550 |

| Kurtosis: | 2.891 | Cond. No. | 6.75e+04 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 6.75e+04. This might indicate that there are

strong multicollinearity or other numerical problems.

smf.ols('goal_difference ~ forward', data=df).fit().summary()

| Dep. Variable: | goal_difference | R-squared: | 0.332 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.295 |

| Method: | Least Squares | F-statistic: | 8.934 |

| Date: | Tue, 03 Sep 2024 | Prob (F-statistic): | 0.00787 |

| Time: | 10:05:32 | Log-Likelihood: | -94.262 |

| No. Observations: | 20 | AIC: | 192.5 |

| Df Residuals: | 18 | BIC: | 194.5 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -25.7248 | 10.698 | -2.405 | 0.027 | -48.200 | -3.250 |

| forward | 0.0007 | 0.000 | 2.989 | 0.008 | 0.000 | 0.001 |

| Omnibus: | 1.089 | Durbin-Watson: | 1.010 |

|---|---|---|---|

| Prob(Omnibus): | 0.580 | Jarque-Bera (JB): | 0.161 |

| Skew: | 0.120 | Prob(JB): | 0.923 |

| Kurtosis: | 3.369 | Cond. No. | 7.23e+04 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 7.23e+04. This might indicate that there are

strong multicollinearity or other numerical problems.

Now we are interesting in taking both defense and forward spending into account at the same time.

This is multiple regression.

Notice that in multiple regression, we calculate the fitted \(\hat{\vec{y}}\) values by adding to together the components due to the first predictor, and that due to the second predictor, and the intercept.

def sse_multi(params, X, y):

""" Multiple regression sum of squared error

Parameters

----------

params : slopes and intercept

X : array

2D array of predictor columns.

y : array

1D array of outcome vector.

Returns

-------

cfv : float

Cost function value

"""

n, p = X.shape

y_hat = np.zeros(n)

for col_no in range(p): # Go through each column.

col = X[:, col_no] # Get the relevant column from X

fit_for_this_col = col * params[col_no] # Multiply by corresponding parameter

y_hat = y_hat + fit_for_this_col

y_hat = y_hat + params[-1] # Add the intercept

errors = y - y_hat

return np.sum(errors ** 2)

We compile the 2D array containing the two predictor columns, by taking two columns out of the data frame, and converting to an array.

X = np.array(df[['defense', 'forward']])

X

array([[ 60320, 74860],

[ 46540, 40352],

[ 51220, 72540],

[ 29516, 43460],

[ 37024, 45350],

[ 60480, 112780],

[ 28860, 27040],

[ 28040, 25440],

[ 17640, 16790],

[ 20736, 26820],

[ 27276, 24040],

[ 20930, 26000],

[ 8686, 9620],

[ 26160, 36470],

[ 12137, 21530],

[ 31512, 39310],

[ 13150, 18144],

[ 14940, 15110],

[ 14880, 9280],

[ 14760, 6280]])

Next we use minimize to find the three parameters that minimize the cost

function. We found that both powell and the default methods gave warnings about failing to reach good results, so we tried the nelder-mead method.

min_res_2 = spo.minimize(sse_multi, [0.001, 0.001, -36],

method='nelder-mead',

args=(X, df['goal_difference']))

min_res_2

message: Optimization terminated successfully.

success: True

status: 0

fun: 8270.703854709001

x: [ 2.933e-03 -8.665e-04 -5.288e+01]

nit: 107

nfev: 192

final_simplex: (array([[ 2.933e-03, -8.665e-04, -5.288e+01],

[ 2.933e-03, -8.665e-04, -5.288e+01],

[ 2.933e-03, -8.665e-04, -5.288e+01],

[ 2.933e-03, -8.665e-04, -5.288e+01]]), array([ 8.271e+03, 8.271e+03, 8.271e+03, 8.271e+03]))

Here are the parameters:

slope for

defenseslope for

attackintercept.

min_res_2.x

array([ 0.002933, -0.000867, -52.875186])

We can do the same parameter estimating using statsmodels in our case, because we are using the standard least-squares cost function.

fitted = smf.ols('goal_difference ~ defense + forward', data=df).fit()

fitted.summary()

| Dep. Variable: | goal_difference | R-squared: | 0.620 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.575 |

| Method: | Least Squares | F-statistic: | 13.85 |

| Date: | Tue, 03 Sep 2024 | Prob (F-statistic): | 0.000270 |

| Time: | 10:05:32 | Log-Likelihood: | -88.626 |

| No. Observations: | 20 | AIC: | 183.3 |

| Df Residuals: | 17 | BIC: | 186.2 |

| Df Model: | 2 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -52.8752 | 11.236 | -4.706 | 0.000 | -76.581 | -29.169 |

| defense | 0.0029 | 0.001 | 3.587 | 0.002 | 0.001 | 0.005 |

| forward | -0.0009 | 0.000 | -1.772 | 0.094 | -0.002 | 0.000 |

| Omnibus: | 1.441 | Durbin-Watson: | 1.303 |

|---|---|---|---|

| Prob(Omnibus): | 0.486 | Jarque-Bera (JB): | 1.207 |

| Skew: | -0.548 | Prob(JB): | 0.547 |

| Kurtosis: | 2.501 | Cond. No. | 1.21e+05 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.21e+05. This might indicate that there are

strong multicollinearity or other numerical problems.

The found parameters are almost exactly what we found with minimize.

fitted.params

Intercept -52.875175

defense 0.002933

forward -0.000867

dtype: float64

The parameters make us think that we gain very little — or even lose — by extra spending on forwards, given a particular level of spending on defense.

Another way of looking at this is to first remove (“regress out”) the effect of spending on defense, leaving the errors (AKA residuals). The residuals are what remains of goal difference after we have done the best job we can (in the least-squares sense) of removing the effect of spending on defense.

defense_only_fit = smf.ols('goal_difference ~ defense', data=df).fit()

defense_only_fit.params

Intercept -45.236577

defense 0.001602

dtype: float64

Here we calculate residuals (errors) left over after using the fit from the defense-only model.

y_hat = defense_only_fit.params['defense'] * df['defense'] + defense_only_fit.params['Intercept']

errors = df['goal_difference'] - y_hat

errors

0 21.613471

1 38.686853

2 6.190233

3 26.956610

4 -1.070019

5 -51.642824

6 8.007419

7 3.320929

8 14.980085

9 7.020783

10 -16.455264

11 15.710025

12 23.322978

13 1.332392

14 1.795021

15 -28.240666

16 -12.827644

17 2.305058

18 -21.598831

19 -39.406610

dtype: float64

In fact Statsmodels is kind enough to calculate these for us, by default, in the resid attribute of the fit.

defense_only_fit.resid

0 21.613471

1 38.686853

2 6.190233

3 26.956610

4 -1.070019

5 -51.642824

6 8.007419

7 3.320929

8 14.980085

9 7.020783

10 -16.455264

11 15.710025

12 23.322978

13 1.332392

14 1.795021

15 -28.240666

16 -12.827644

17 2.305058

18 -21.598831

19 -39.406610

dtype: float64

We can take the residual — left over — values, and put them back into the data frame, so Statmodels can do another fit.

df['without_defense'] = fitted.resid

df

| rank | team | played | won | drawn | lost | for | against | goal_difference | points | wages_year | keeper | defense | midfield | forward | without_defense | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | Manchester City | 38 | 29 | 6 | 3 | 99 | 26 | 73 | 93 | 168572 | 8892 | 60320 | 24500 | 74860 | 13.837431 |

| 1 | 2 | Liverpool | 38 | 28 | 8 | 2 | 94 | 26 | 68 | 92 | 148772 | 14560 | 46540 | 47320 | 40352 | 19.349313 |

| 2 | 3 | Chelsea | 38 | 21 | 11 | 6 | 76 | 33 | 43 | 74 | 187340 | 12480 | 51220 | 51100 | 72540 | 8.515417 |

| 3 | 4 | Tottenham Hotspur | 38 | 22 | 5 | 11 | 69 | 40 | 29 | 71 | 110416 | 6760 | 29516 | 30680 | 43460 | 32.970125 |

| 4 | 5 | Arsenal | 38 | 22 | 3 | 13 | 61 | 48 | 13 | 69 | 118074 | 8400 | 37024 | 27300 | 45350 | -3.411476 |

| 5 | 6 | Manchester United | 38 | 16 | 10 | 12 | 57 | 57 | 0 | 58 | 238780 | 28600 | 60480 | 36920 | 112780 | -26.773404 |

| 6 | 7 | West Ham United | 38 | 16 | 8 | 14 | 60 | 51 | 9 | 56 | 77936 | 11856 | 28860 | 10180 | 27040 | 0.665784 |

| 7 | 8 | Leicester City | 38 | 14 | 10 | 14 | 62 | 59 | 3 | 52 | 81590 | 10040 | 28040 | 18070 | 25440 | -4.315766 |

| 8 | 9 | Brighton and Hove Albion | 38 | 12 | 15 | 11 | 42 | 44 | -2 | 51 | 49820 | 3120 | 17640 | 12270 | 16790 | 13.689769 |

| 9 | 10 | Wolverhampton Wanderers | 38 | 15 | 6 | 17 | 38 | 43 | -5 | 51 | 62756 | 2120 | 20736 | 13080 | 26820 | 10.301066 |

| 10 | 11 | Newcastle United | 38 | 13 | 10 | 15 | 44 | 62 | -18 | 49 | 73308 | 4940 | 27276 | 17052 | 24040 | -24.288248 |

| 11 | 12 | Crystal Palace | 38 | 11 | 15 | 12 | 50 | 46 | 4 | 48 | 71910 | 6000 | 20930 | 18980 | 26000 | 18.021561 |

| 12 | 13 | Brentford | 38 | 13 | 7 | 18 | 48 | 56 | -8 | 46 | 28606 | 2080 | 8686 | 8220 | 9620 | 27.736951 |

| 13 | 14 | Aston Villa | 38 | 13 | 6 | 19 | 52 | 54 | -2 | 45 | 85330 | 8320 | 26160 | 14380 | 36470 | 5.755570 |

| 14 | 15 | Southampton | 38 | 9 | 13 | 16 | 43 | 67 | -24 | 40 | 58657 | 9270 | 12137 | 15720 | 21530 | 11.936166 |

| 15 | 16 | Everton | 38 | 11 | 6 | 21 | 43 | 66 | -23 | 39 | 110202 | 8060 | 31512 | 31320 | 39310 | -28.479761 |

| 16 | 17 | Leeds United | 38 | 9 | 11 | 18 | 42 | 79 | -37 | 38 | 37354 | 2080 | 13150 | 3980 | 18144 | -6.968775 |

| 17 | 18 | Burnley | 38 | 7 | 14 | 17 | 34 | 53 | -19 | 35 | 40830 | 2900 | 14940 | 7880 | 15110 | 3.152527 |

| 18 | 19 | Watford | 38 | 6 | 5 | 27 | 34 | 77 | -43 | 23 | 42030 | 2580 | 14880 | 15290 | 9280 | -25.723314 |

| 19 | 20 | Norwich City | 38 | 5 | 7 | 26 | 23 | 84 | -61 | 22 | 31750 | 3480 | 14760 | 7230 | 6280 | -45.970937 |

Now we look to see if the forward spending can predict what is left over, after taking into account the effect of defense spending on goal difference:

smf.ols('without_defense ~ forward', data=df).fit().summary()

| Dep. Variable: | without_defense | R-squared: | 0.000 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | -0.056 |

| Method: | Least Squares | F-statistic: | 0.000 |

| Date: | Tue, 03 Sep 2024 | Prob (F-statistic): | 1.00 |

| Time: | 10:05:32 | Log-Likelihood: | -88.626 |

| No. Observations: | 20 | AIC: | 181.3 |

| Df Residuals: | 18 | BIC: | 183.2 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -1.288e-14 | 8.071 | -1.6e-15 | 1.000 | -16.956 | 16.956 |

| forward | -1.335e-18 | 0.000 | -7.11e-15 | 1.000 | -0.000 | 0.000 |

| Omnibus: | 1.441 | Durbin-Watson: | 1.303 |

|---|---|---|---|

| Prob(Omnibus): | 0.486 | Jarque-Bera (JB): | 1.207 |

| Skew: | -0.548 | Prob(JB): | 0.547 |

| Kurtosis: | 2.501 | Cond. No. | 7.23e+04 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 7.23e+04. This might indicate that there are

strong multicollinearity or other numerical problems.

It appears that this two-stage procedure gives a similar result to the one we saw before — once we have accounted for spending on defense, spending on forwards is no longer important, in these models.